Lets take our regular look at six of the main US indexes

sp'500

Despite the SPX ending the week on a very positive note, it still made for a third consecutive net weekly decline, settling -30pts (1.0%) to 2888. Note last week's break of m/t rising trend, which offers further cooling to at least the lower bollinger, which will be around the 2800 threshold next week. Price momentum is increasingly negative, having ticked lower for a third week.

Nasdaq comp'

A third week lower for tech, settling -63pts (0.8%) at 7895.

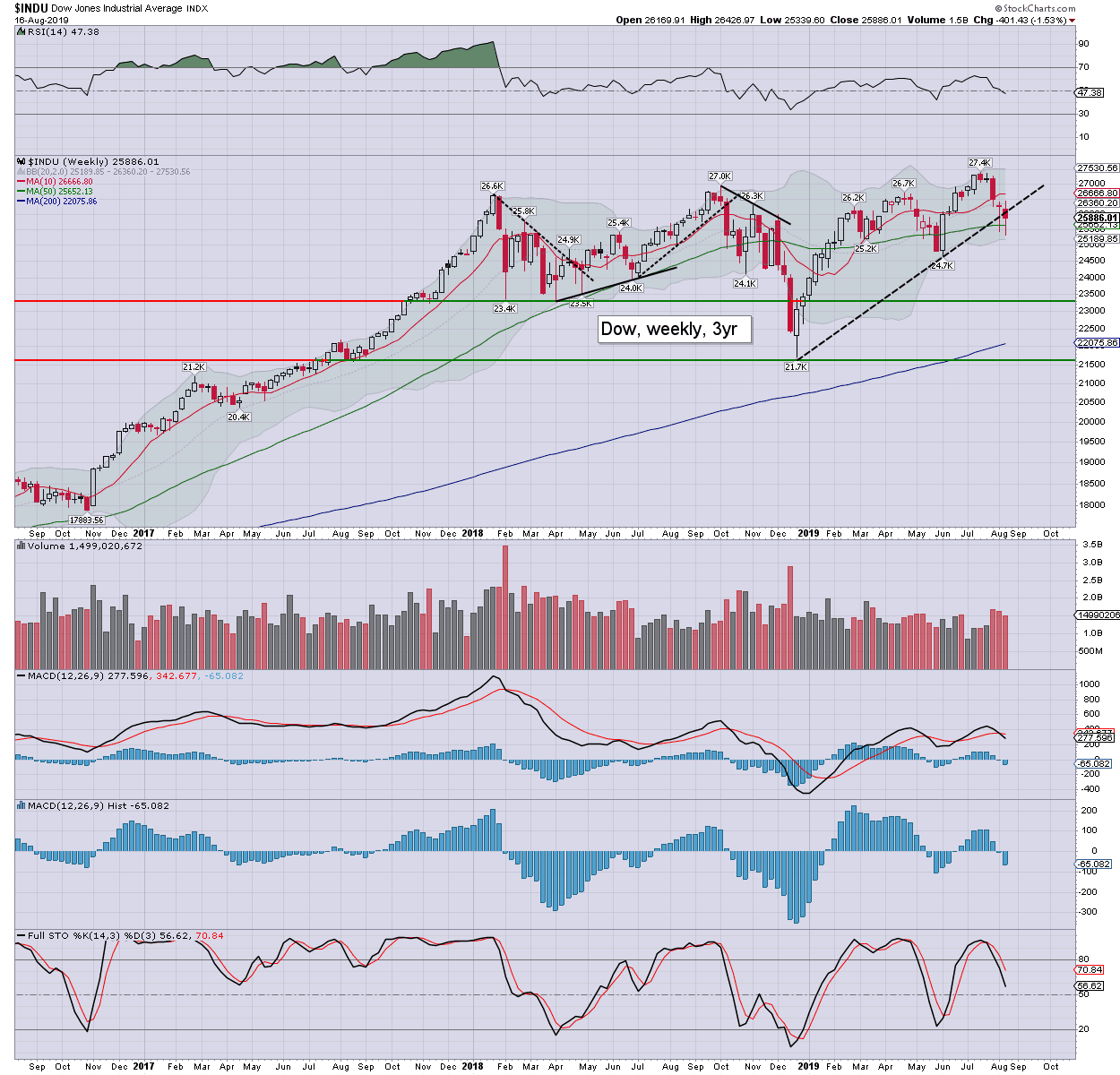

Dow

The mighty Dow fell for the 4th week of 5, settling -401pts (1.5%) to 25886. The s/t outlook is bearish, with first support of the June low of 24680.

NYSE comp'

The master index cooled for the 4th week of 5, settling -168pts (1.3%) to 12580. The May low of 12238 isn't much further down.

R2K

The second market leader fell for a third consecutive week, settling -19pts (1.3%) to 1493.

Trans

The 'old leader' - Transports, lead the way lower this week, settling -239pts (2.3%) to 9967. Weekly technicals are all leaning bearish, and offer the June low of 9715, with secondary support of the 9400s.

–

Summary

All six US equity indexes settled net lower for the week.

The Transports lead the way lower, whilst the Nasdaq comp' was most resilient.

Last week's break of m/t rising trend offers further downside to the June lows.

--

Looking ahead

Another busy week can be expected. The market will continue to give some attention to the China/HK situation, whilst also dealing with further earnings, econ-data, and some central bankers at Jackson Hole.

Earnings:

M - BIDU, WB, SINA, IQIYI, BHP

T - HD, KSS, CREE, URBN, TOL

W - TGT, LOW, ADI, JWN, LB

T - CRM, VMW, GPS, HPQ

F - FL

-

Econ-data:

M -

T -

W - Existing home sales, EIA Pet', FOMC mins (2pm)

T - Weekly jobs, Leading indi'

F - New home sales

*Thurs/Friday: Jackson Hole, Wyoming, where a number of global central bankers will be meeting. The event will receive considerable attention from the media. Sporadic comments can be expected across the two days, although no major policy announcements can be expected.

--

Final note

Recent equity price action has been pretty wild, although the VIX hasn't seen any kind of hyper spike. Its arguable another push lower to the June equity lows might offer such a volatility spike, before better chance of an equity rally. New historic highs look unlikely any time soon. The following merits regular consideration...

Fed rates with SPX, monthly, 20yr

*the July rate cut hasn't yet been factored into what is an eom (end of month) chart.

The recently added red vertical line is not to be dismissed lightly. It is my guess we'll see a rate cut at each of the remaining three FOMCs this year (Sept'18th, Oct'30th, Dec'11th). I expect the fed to cut by -25bps each meeting, taking rates to 1.25/1.50% by year end.

Even some within the mainstream now expect rates to return to zero in 2020 or 2021. We're clearly also going to see QE4. Perhaps the only unknown is whether that is initiated by Powell or Bullard. In either case, there will be massive implications for everything, not least the precious metals and related mining stocks.

Ohh, and no, I don't see the situation as analogous to 1998. The econ-data is coming in increasingly weak, especially across Europe. One thing should be crystal clear, lower rates are not going to help avert a recession.

--

If you value my work on Blogger and Twitter, subscribe to me.

For details/latest offers, see: Permabeardoomster.com

Have a good weekend

--

*the next post on this page will likely appear 5pm EDT on Monday.