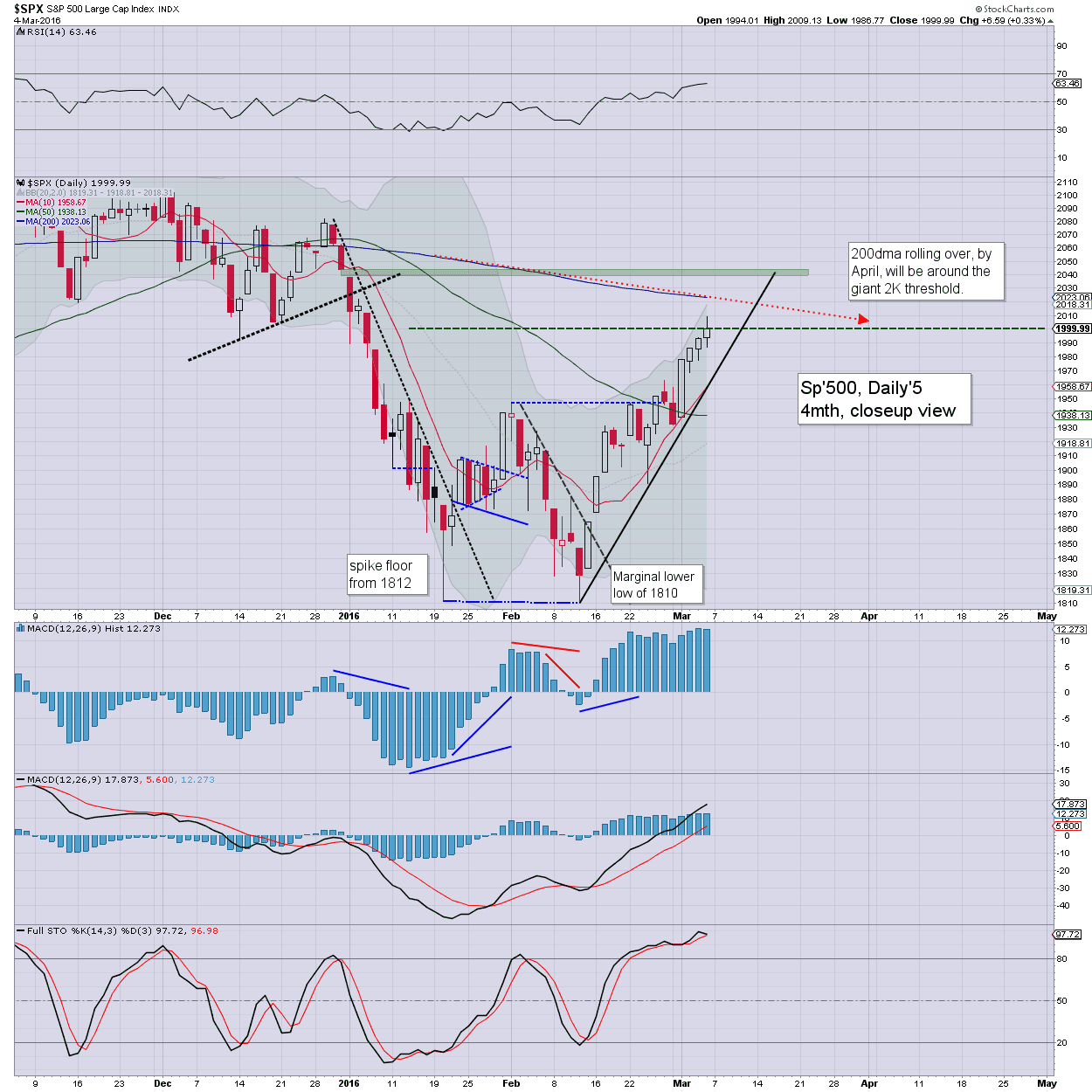

Lets take our monthly look at ten of the world equity markets

USA - Dow

The Dow swung from an intra month low of 15503, to settle +50pts (0.3%) @ 16516. With a Friday close of 17006, the bulls have managed a notable weekly close above the 17K threshold.

The monthly 10MA stands at 17092. Arguably, the equity bears should seek a March close back under 17K, preferably <16500.

First big downside target for the spring will be a break below the Aug'2015 low of 15370, and then the 14200/000 zone. From there, the 13500/400 zone, which seems the most realistic 'best bear' case by June.

Germany

The economic powerhouse of the EU - Germany, saw a third consecutive monthly fall, with a Feb' decline of -3.1%. The DAX has already come pretty close to testing rising support of 8500. Equity bears seeking grander downside across 2016, should be looking for a monthly close under 8K. If that is attained, next target would be the 7000/6500 zone.

Japan

The Nikkei saw a fiercely bearish Feb', and despite climbing into end month, still fell a net -8.5%. First resistance is the 18500/18k zone. Renewed downside to 12K looks probable by June.

China

The Shanghai comp' fell a net -8.1%, having hit a fractional new cycle low of 2638. First upside resistance is the 3250/3000 zone. Renewed downside to 2000 looks due. How the communist leadership will react to such a 60% decline from the summer 2015 high... is another matter entirely.

Brazil

The Brazilian market had a relatively strong month, settling +5.9% in the 42000s. First upside resistance is the 49/50k zone. If renewed upset across world capital markets this spring/summer, the Bovespa looks set to hit the 30K threshold, which is a clear 28% or so lower.

Russia

With energy prices pushing higher into end month, the Russian market managed a net gain of 3.4% to 766. There is strong resistance at the 10MA of 817.. which was where the market closed on Friday. If oil/gas prices see renewed downside (as seems probable), first downside target will be the 550/500 zone.

UK

The FTSE managed a fractional net monthly gain of 0.2% @ 6097. First resistance is the 6300/250 zone. If renewed market downside, first target is the 5000/4750 zone.

France

The French CAC saw a net decline of -1.4%, settling in the 4300s. First upside resistance is the 4600/500 zone. If a failure to clear/hold, then next downside target is 3500.

Spain

The ugliest of the EU-PIIGS - Spain, saw a net monthly decline of -4.0% to 8461. First upside resistance is the 9800/500 zone. Renewed weakness would see the IBEX probably implode to around 6000.

Greece

The economic/societal basket-case of the EU - Greece, saw a fourth consecutive monthly decline, settling -6.5% @ 516, having broken a new multi-decade low of 420. If world equity markets see renewed broad downside, the Athex looks set for the 300/250 zone.

I have long wondered that if the Greeks decided to abandon the Euro, if we'd eventually see the Athex go sub 100. That still seems possible, as the current trend from spring 2014 is very bearish.

--

Summary

February saw many world equity markets break new multi-year lows. Despite a rebound into end month, and across the first four days of March, the broader trend remains bearish.

What is now critically important is whether world equity markets are going to put in another lower high, and rollover.. or keep on pushing higher into April/May.

From a pure technical perspective, continued upside for another few months seems very unlikely.

From a economic/financial system perspective, there are a great many problems, not least of which is that we are yet to see capitulation in the oil/gas/mining/shipping sectors.

There are all sorts of counter-party and derivative issues, any one of which could cause great upset to world capital markets.

.. and no doubt, if such events occurred, the central banks would try to paper over the widening cracks with even more QE.. or far far worse................ NIRP, as the ECB and BoJ have already resorted to.

--

Looking ahead

There is very little of significance scheduled in the week ahead, except for the ECB meeting.

M - Consumer credit, Fed official Fischer is due to speak in the afternoon

T - -

W - Wholesale trade, EIA report

T - weekly jobs, US Treasury Budget

*the ECB will issue a policy statement around 7am EST, with a Draghi press conf' at 8.30am EST.

F - import/export prices

--

Back on Monday :)