Lets take our regular look at six of the main US indexes

sp'500

A net weekly decline of -34pts (1.2%) to settle at 2752. Range 2801/2741. Near term outlook offers a little chop ahead of the fed. A March close >2800 looks increasingly probable, with a break to new historic highs in late April/early May. Big target is the 2950/3047 zone, which is where the sp' will be extremely likely to become stuck.

--

Nasdaq comp'

The Nasdaq broke new historic highs on Monday and Tuesday, the latter seeing 7637. The 8000s look on the menu this spring/early summer. Key tech stocks: INTC, CSCO, MU, NVDA.

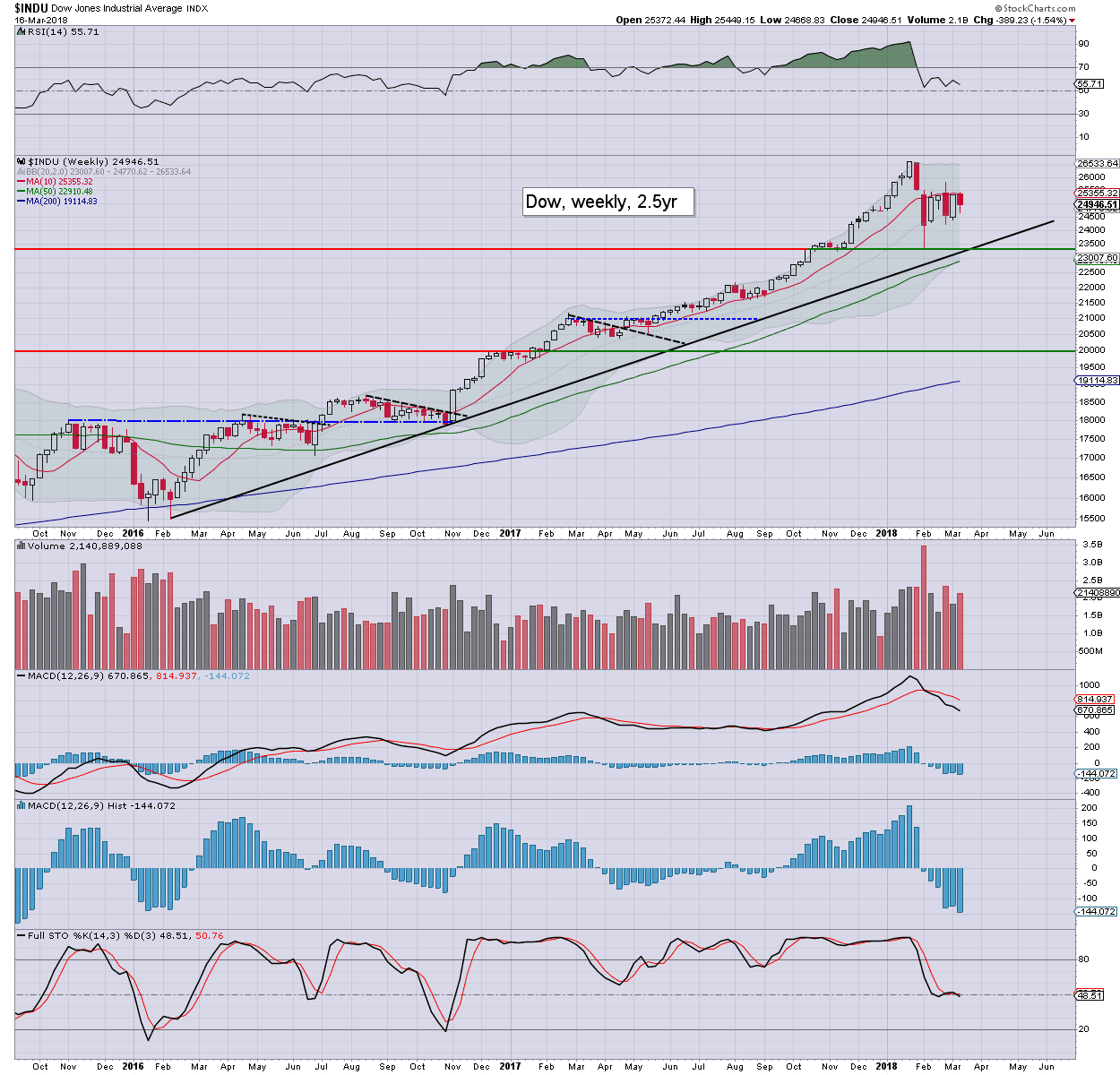

Dow

The mighty Dow was the biggest decliner this week, -1.5% at 24946. Note how the key 10MA is acting as some degree of resistance. Equity bulls should be seeking a monthly close >25500 to give confidence that new historic highs are coming by early summer.

NYSE comp'

The master index cooled by -1.0% to 12784. Underlying MACD (blue bar histogram) cycle remains on the low side. A multi-week up wave is due, that should last into May/June.

R2K

The second market leader saw a moderate net weekly decline of -0.7%. The R2K came very close - intra high 1609, to breaking a new historic high (1615). Upper bollinger offers the 1620/30s before end March.

Trans

The 'old leader' was rather resilient this week, seeing a moderate decline of -0.5%. Equity bulls should be seeking a weekly close >10800s to give confidence that new historic highs are coming by early summer. It should be kept in mind that any spring/summer surge in oil/fuel prices would be a particularly downward pressure on the transportation stocks.

–

Summary

All six of the US equity indexes saw net weekly declines.

The Dow lead the way lower, whilst the two leaders: Trans/R2K, were more resilient.

Notably, the Nasdaq comp' broke consecutive new historic highs on Monday and Tuesday, with the R2K coming rather close. It gives some confidence to the notion that the broader market will climb across the spring, and into early summer.

--

Looking ahead

Earnings: ORCL (Mon'), FDX (Tues'), MU, KBH (Thurs')

M -

T -

W - Existing home sales, EIA Pet' report.

The FOMC will issue a press release at 2pm. That will detail a rate hike of 25bps to a new target range of 1.50-1.75%. There will be a press conf' with new Fed chair Powell at 2.30pm, and that will likely last a full hour.

T - Weekly jobs, FHFA house price index, leading indicators

F - Durable goods orders, new home sales

*Other than Powell on Wednesday, the only other fed officials on the loose will be Bostic and Kashkari. The latter remains notably against any rate hikes.

--

If you value my work, subscribe to me.

For details: https://permabeardoomster.blogspot.co.uk/p/subscriptions.html

Have a good weekend

--

*the next post on this page will likely appear 6pm EST on Monday.