Lets take our regular look at six of the main US indexes (monthly candle charts)

sp'500

The sp'500 saw a net weekly gain of 58pts (2.1%) to settle at 2892. More broadly, the macd (blue bar histogram) cycle continues to tick upward, as momentum is swinging back toward the bulls. A bullish cross is due late May/June. New historic highs >2940 are on the menu. The next key Fibonacci extrapolation is the 2.618x of 3047, and that is only another 155pts (5.4%) to the upside.

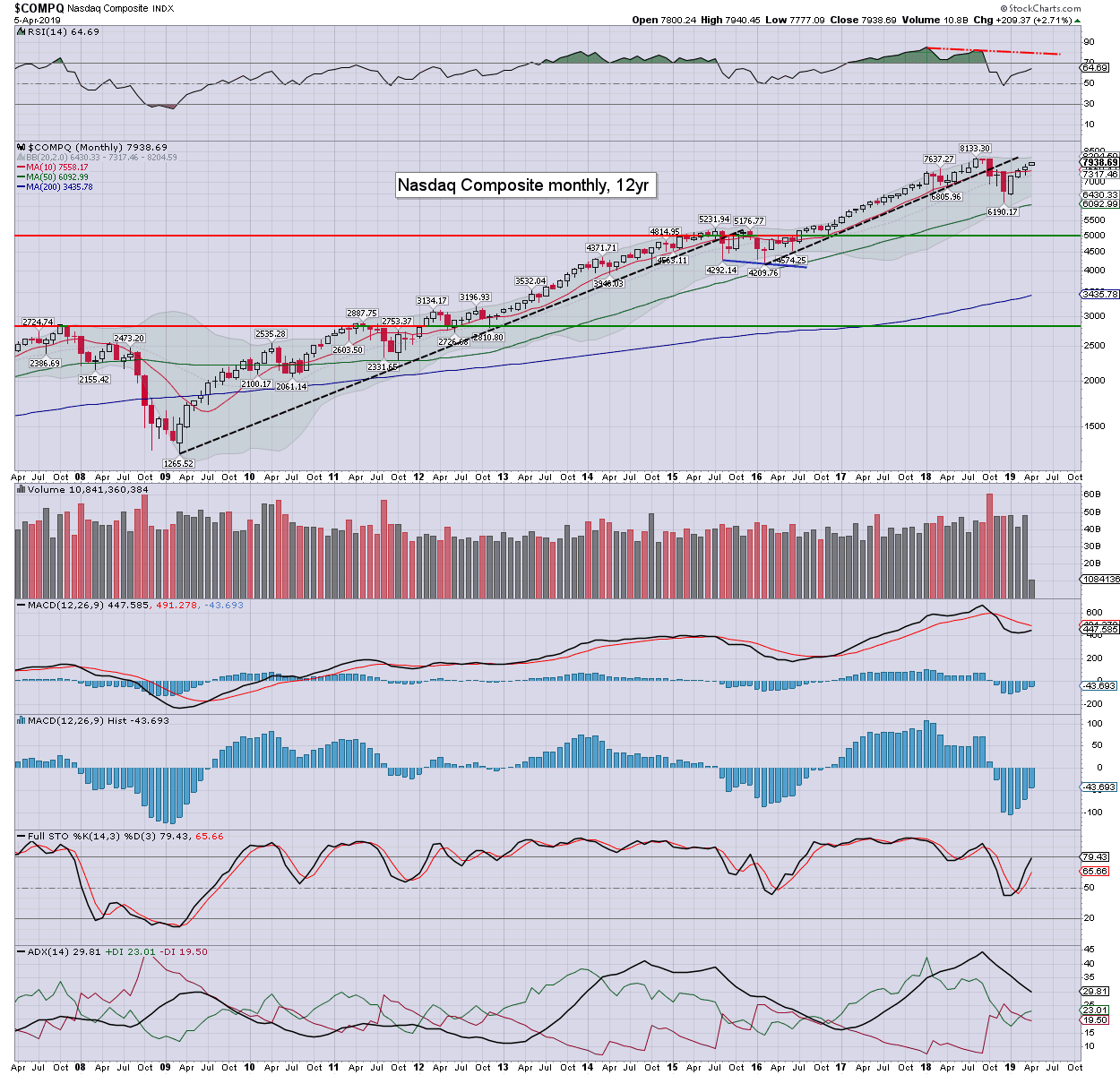

Nasdaq comp'

The Nasdaq saw a net weekly gain of 209pts (2.7%) to 7938. At the current rate, monthly price momentum will turn positive late May/early June. New historic highs >8133 appear probable, with key leadership from MSFT and CSCO.

Dow

The mighty Dow saw a net weekly gain of 496pts (1.9%) to 26424. New historic highs >26951 appear probable. Its notable that the Dow has already broken the 2.618x fib' of 26702 in Sept'2018.

NYSE comp'

The master index climbed 230pts (1.8%) to 12927. The next key level is the Sept'2018 high of 13261. If that can be broken above, it will bode strongly for the broader market into the summer.

R2K

The second market leader gained 42pts (2.8%) to 1582. If the April settlement is above the key 10MA - currently at 1569, it will offer new historic highs this summer.

Trans

The 'old leader' - Transports, was the leader this week, +326pts (3.1%) to 10734, notably back above the key 10MA. Considering the sustained push higher in WTIC/fuel prices, the strength in the Transports is even stronger than might be initially recognised.

–

Summary

All six of the main indexes saw significant net weekly gains.

The Transports and R2K are leading the way higher, with the NYSE comp' lagging.

All six of the main indexes are trading above their respective monthly 10MA.

YTD price performance:

The Nasdaq comp' is leading the way, currently +19.6% for the year. The R2K is +17.3%, the Transports +17.0%, and the SPX +15.4%. The NYSE comp' is +13.7%, with the Dow lagging, but still higher by a very respectable +13.3%.

--

Looking ahead

Earnings: DAL, BBBY (Wed'), JPM, WFC, PNC (Fri').

*Disney will have an analyst meeting on Thursday, and that will capture some mainstream attention, not least after the recently finalised purchase of various FOX assets. The movie/TV franchises of Marvel and Star Wars will no doubt be highlighted, both of which are money making machines. An update on the planned streaming service can be expected, which should spook the Netflix bulls.

-

M - Factory orders

T -

W - CPI, EIA Pet' report, FOMC mins (2pm)

T - PPI, Weekly jobs

F - Import/export prices, consumer sent'.

*Fed chair Powell is due to speak about the economy at the House of Representatives Democratic Caucus annual retreat in Virginia. That event will span Wed>Fri', and I'm unaware if it will garner any live coverage.

**Fed officials Bullard and Williams are due on Thursday, and some of their remarks will probably catch Mr Market's attention.

***Friday is (at least currently) set to be BREXIT day, with the UK set to exit the EU, with... or without a deal. Its possible that might be delayed to late June... or just cancelled entirely.

--

Final note

It was another week for the equity bulls, as new historic highs aren't far off now. Even the Transports and R2K - which saw bearish March settlements, have pushed above key thresholds. As things are, the bulls look set to control things across the spring, if not all the way into late Summer.

The US econ-data, whilst weaker relative to Q4, is still coming in far from recessionary. Things continue to deteriorate elsewhere, but even German equities are battling upward.

The QT program is set to conclude in September, and from there, it is just a matter of whether rate cut'1 is seen at the FOMC of Oct'30th or Dec'11th. Regardless of which it is, for yours truly, such a rate cut will merit as being the ultimate sell signal, just as it was in Sept'2007.

--

If you value my work on Blogger and Twitter, subscribe to me.

For details/latest offers, see: Permabeardoomster.com

Have a good weekend

--

*the next post on this page will likely appear 5pm EDT on Monday.