sp'daily5

VIX'daily3

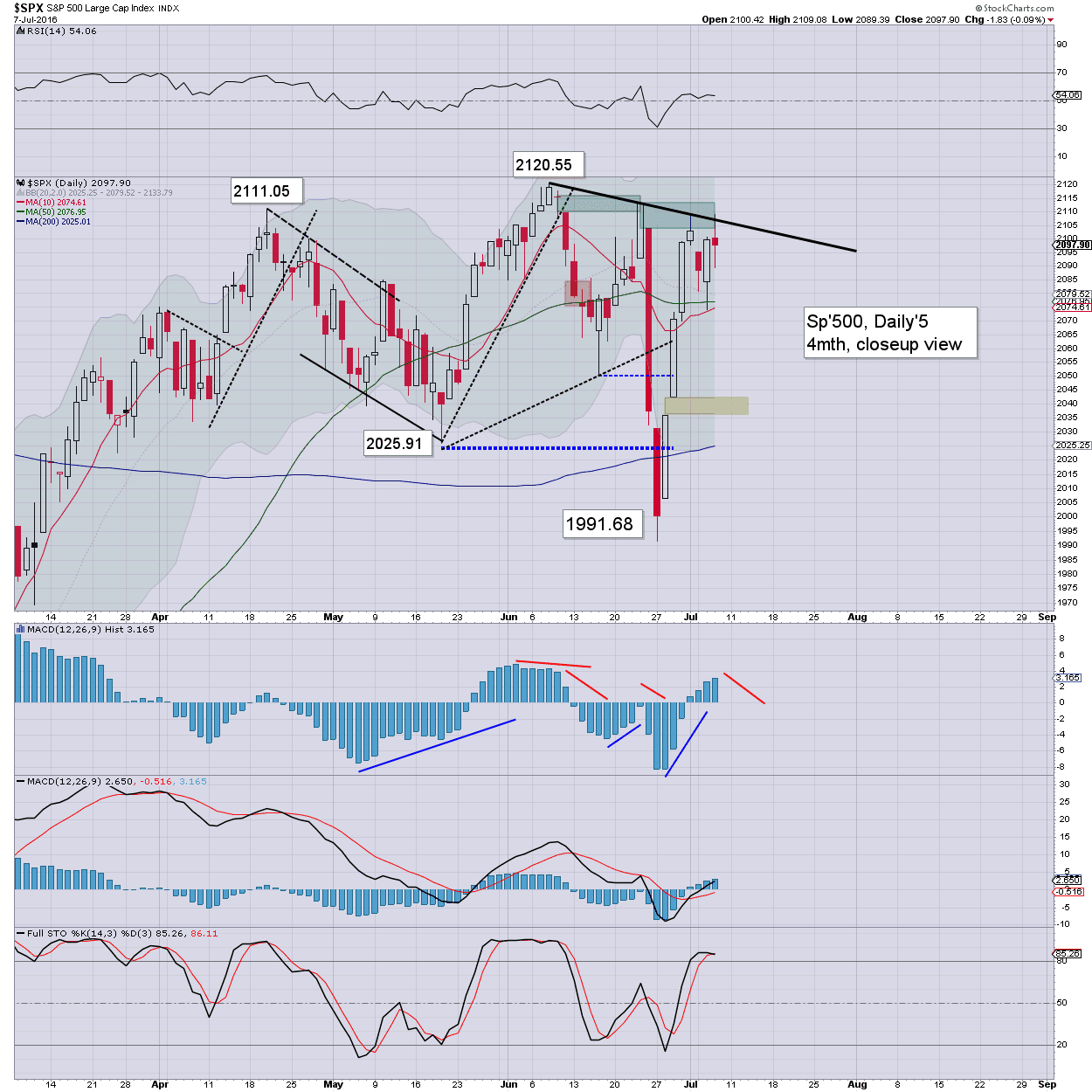

Summary

The morning high of sp'2109 was just another tease to those who still believe we're in a bull market. Arguably, today saw failure number 18, since the May 2015 high of 2134.

--

VIX remains relatively subdued, but as this afternoon showed, any degree of equity weakness will see the VIX jump pretty quickly.

From a pure cyclical perspective, equities are more likely to break lower.. than up and away.

--

More bad news?

The US capital markets await the latest employment data from the BLS. Regardless of whatever numbers are issued, what will matter is how the market interprets the data.

My guess is 90-110k net gains, but even if that is correct, would the market decide that 'bad news is bad news' or 'bad news is good news', in that a rate rise could be ruled out for the remainder of the year?

Anyway, besides the US data, the financial tremors continue to grow in the EU, and that can't just be dismissed as 'not important' by the equity bull maniacs.

notable weakness, DB, daily

A net daily decline of -3.2% to $12.56, but hey... its nothing to be worried about, right?

Goodnight from London