It was a bearish week for US equity indexes,

with net weekly declines ranging from -2.5%

(R2K), -2.2% (Nasdaq comp'), -1.1% (Trans), -1.0% (SPX), -0.9% (NYSE comp'), to

-0.4% (Dow). Near term outlook offers another 1-2% of cooling.

Lets take our regular look at six of the main US indexes

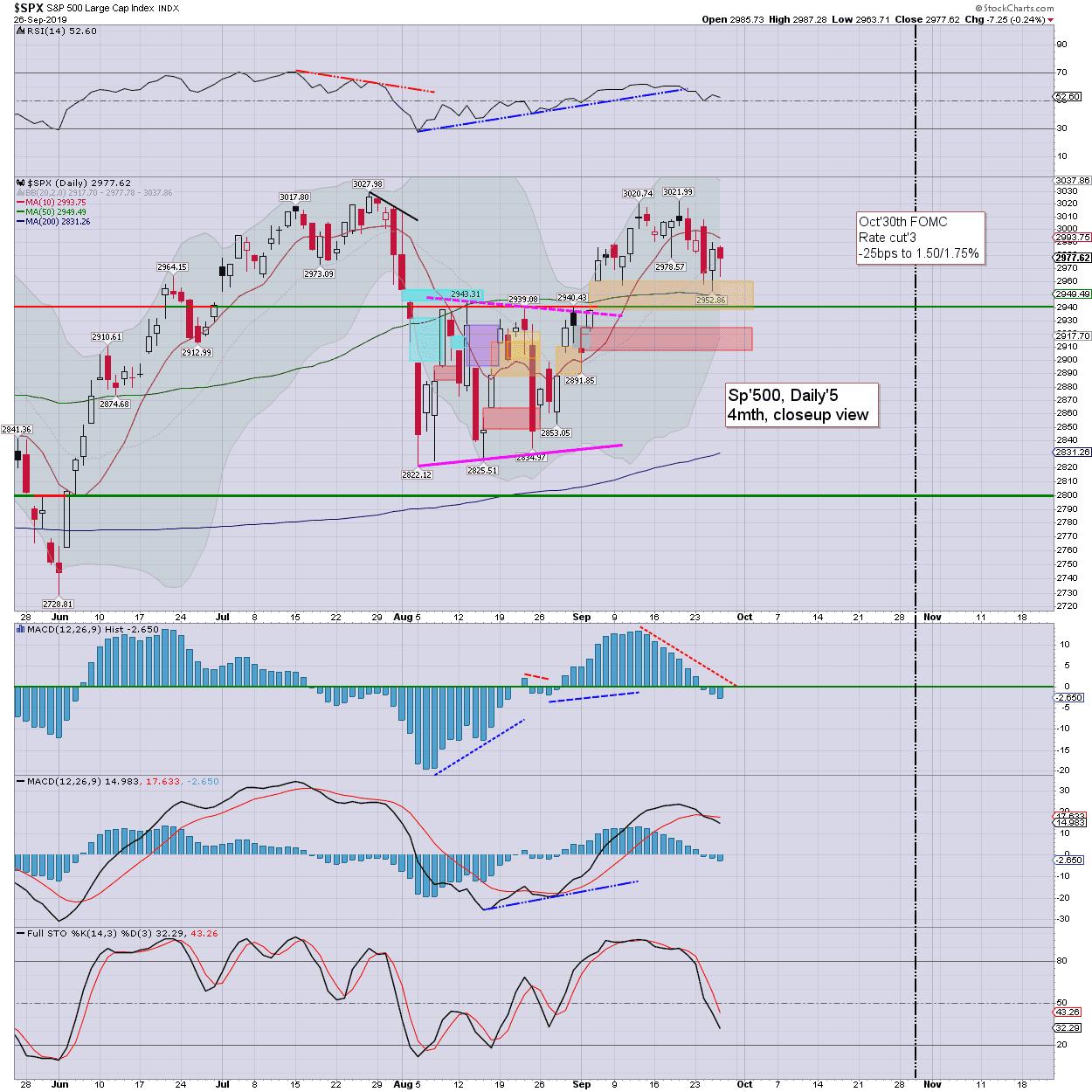

sp'500

The SPX cooled for a second consecutive week, -30pt (1.0%) to 2961. Weekly price momentum ticked back lower, and remains fractionally negative. Note the August low of 2822, which is just under the monthly 10MA (2833). Best guess: cooling to the 2920s, but then finding a floor, and resuming upward. Alarm bells if any daily close <2900 and/or VIX >20.00.

--

Nasdaq comp'

A second week lower for tech, settling -178pts (2.2%) to 7939. Note the settlement under the key 10MA, which threatens a test of the August low of 7662. Weekly price momentum ticked back lower, having failed to re-take the key zero threshold.

Dow

The mighty Dow settled -114pts (0.4%) to 26820. Weekly price momentum remained fractionally positive for a second week.

NYSE comp'

The master index cooled for a second week, settling -121pts (0.9%) to 12971. Price structure since February could be argued is a giant H/S formation. Equity bears would need to see at least the 12500s to keep that scenario/structure valid. Like most other indexes, price momentum has stalled at the zero threshold.

R2K

The second market leader settled -39pts (2.5%) to 1520. Weekly price momentum ticked lower, but remains fractionally positive. I would note the four key cycle highs of 1602, 1618, 1599, and 1590.

Note m/t rising trend from Dec'2018, which was broken in early August. We have effectively back-tested the old broken trend, and have resumed lower. Its 'curious', and threatens a serious break under key price threshold of the 1430s. Its something most will have overlooked.

Trans

The 'old leader' - Transports, settled -113pts (1.1%) at 10341. Weekly price momentum ticked lower, but remains fractionally positive. Price structure is rather similar to the R2K, as the US market has been broadly stuck since early 2018.

–

Summary

All six of the US equity indexes saw net weekly declines.

The R2K and Nasdaq lead the way lower, with the Dow most resilient.

More broadly, all six indexes are currently above their respective monthly 10MA.

YTD price performance:

The Nasdaq comp' continues to lead for the year, currently +19.7%. The SPX is +18.1%, the Dow +15.0%, with the NYSE comp' +14.0%. The Transports are +12.8%, and the R2K +12.7%.

--

Looking ahead

Earnings: LEN, BBBY (Wed'), PEP, STZ (Thurs').

Econ-data:

M - Chicago PMI

T - PMI/ISM manu', construction

W - Vehicle sales, ADP jobs, EIA Pet'

T - Weekly jobs, PMI/ISM serv', factory orders

F - Monthly jobs, intl' trade

*Monday will be end month/Q3. I would expect higher volume, with more dynamic price action.

--

Final note

Whilst the s/t outlook offers a little further cooling, it should be clear, the US equity market and economy is still pretty strong. All the main indexes are holding m/t bullish trends.

Just so there is no misunderstanding...

SPX, monthly'5, fib' levels

First, the current m/t trend IS bullish. That would arguably only change with a monthly settlement under the key 10MA, currently at 2833.

Note the next giant Fibonacci extrapolation of 3047. If we break above that, then I would have to seek far higher levels in 2020/21, arguably to at least 3900/4000. Whilst that might sound crazy, the crazy train does already have some passengers...

If we do break above 3047, Lee's hyper bullish call will have to be seen as one of the best market calls in some years.

Arguing against such upside are the bond and precious metals markets. Those signals would only be negated if the US 10yr >2.25%, and Gold <$1370s. Neither of those appear likely before year end. As ever, one day at a time.

If you value my work on Blogger and Twitter, subscribe to me.

For details/latest offers, see:

Permabeardoomster.com

Have a good weekend

--

*the next post on this page will likely appear 5pm EDT on Monday.