It was a very bullish week for US equity indexes,

with net weekly gains ranging from +4.0%

(Trans), +3.0% (Dow), +2.9% (SPX), +2.7% (Nasdaq comp'), +2.6% (NYSE comp'), to

+2.4% (R2K). Near term outlook offers cooling into end month.

Lets take our regular look at six of the main US indexes (monthly candle charts)

sp'500

The spx climbed for a fourth consecutive week, breaking a new cycle high of 2675, settling +2.9% at 2670. More broadly, the spx is currently net higher for January by +163pts (6.5%). Despite the current gain, macd (blue bar histogram) cycle continues to tick lower, as price momentum is at levels last seen in Feb'2016. Note the key 10MA, a mere 65pts to the upside at 2735. Until that is cleared and held above, the m/t trend is arguably still bearish.

Nasdaq comp'

The Nasdaq comp' saw a very sig' net weekly gain of 2.7% to 7157. Price momentum is at levels last seen in Feb'2009, and is supportive of the notion that the cooling from Aug>Dec'2018 is not comparable to 2015/16 or the 2011 down wave. Note the 10MA at 7427, just 3.8% higher.

Dow

The mighty Dow saw a powerful net weekly gain of 3.0%, settling at 24706. Monthly price momentum continues to favour the bears. Note the key 10MA at 24937, just under 1% higher.

NYSE comp'

The master index saw a net weekly gain of 2.6% to 12151. Price momentum is at levels last seen in March 2016. It is far less supportive to the bearish case, and does threaten that late 2018 cooling was comparable to 2015/16 and 2011.

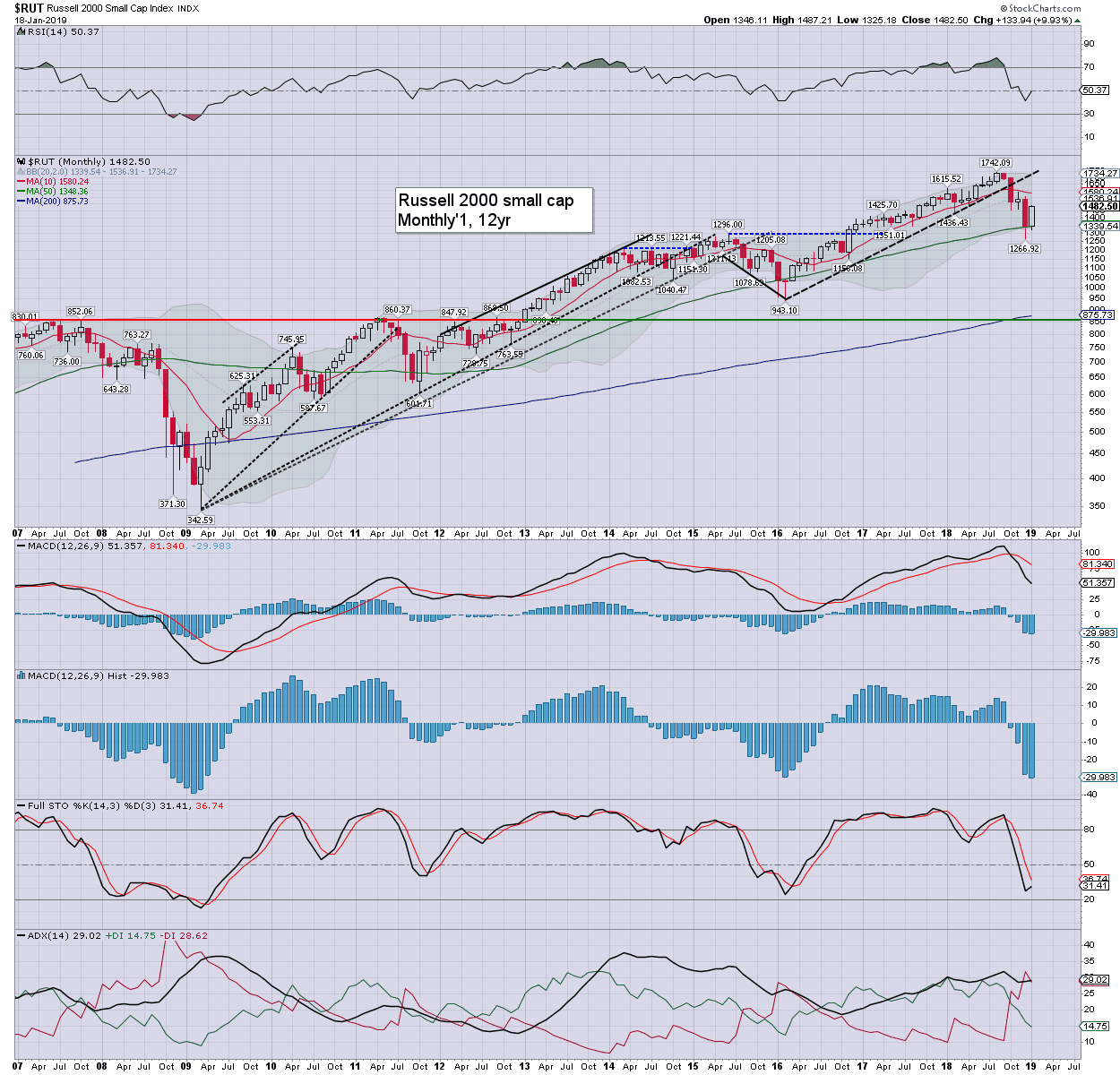

R2K

The second market leader saw a net weekly gain of 2.4% to 1482. Price momentum is around levels last seen in Feb'2016. Note the key 10MA at 1580, which is another 6.2% to the upside.

Trans

The 'old leader' - Transports, lead the way higher this week, with a very powerful gain of 4.0% to 10012. Price momentum is at levels last seen in March 2016. Note the key 10MA at 10547, some 5% higher.

–

Summary

All six equity indexes saw very significant net weekly gains, lead higher by the Transports and Dow.

All six equity indexes are currently net higher for the year, lead by the R2K and Transports.

YTD price performance:

The R2K is currently leading the way, +9.9%, Trans +9.2%, with the Nasdaq comp' +7.9%. The NYSE comp' +6.8%, the SPX +6.5%, and the Dow +5.9%

--

Looking ahead

It will be a short four day trading week.

Key earnings: IBM (Tues'), LVS, UTX, PG, F (Wed'), AAL, FCX, SBUX, INTC (Thurs')

--

M - CLOSED

T - Existing home sales

W - House price index, Richmond Fed'

T - Weekly jobs, leading indicators, EIA Pet' & NG reports

F - Durable goods, new home sales

*The world economic forum will be meeting at Davos in Switzerland, and that will span Jan'22-25. Notably, Trump, May, and Macron will not be attending. Details:

https://www.weforum.org

**As there will be an FOMC Jan'29/30th, there will no fed officials on the loose, due to the usual blackout period.

--

If you value my work on Blogger and Twitter, subscribe to me.

For details and the latest offers:

permabeardoomster.com

Enjoy the three day holiday break.

--

*the next post on this page will likely appear 5pm EST on Tuesday.