It was a broadly bullish week for US equity indexes,

with net weekly changes ranging from +2.3%

(Nasdaq comp'), +2.2% (sp'500), +0.6 (R2K), to -1.6% (Transports). Near term outlook offers further upside to the sp'2950/3047 zone, where the market will very likely get stuck.

Lets take our regular look at six of the main US indexes

sp'500

The sp' climbed for a fourth consecutive week, +62pts (2.2%), settling at a new historic high of 2872. RSI is 90, which is the highest since at least 1980. Underlying MACD (blue bar histogram) cycle is the highest since summer 2009.

Best guess: continued upside to the 2950/3047 zone, where there will be multiple key aspects of resistance. A correction of 5% is clearly overdue, before resuming upward. The year end target of 3245 is on track.

Equity bears have nothing to tout unless a bearish monthly close. For me, that would equate to a monthly close under the key monthly 10MA. That currently stands at 2545, and is rising around 50pts a month. So, at the June 1'st open, key support will be around 2800. I do not expect any such bearish monthly closes this year.

--

Nasdaq comp'

The tech gained a powerful 2.3%, breaking a new historic high of 7505. The 8000s are clearly viable by mid year, with the 9000s for year end. Earnings from Intel were superb, and give m/t confidence.

Dow

The mighty Dow climbed 545pts (2.1%), settling at a new historic high of 26616. RSI is a screeching 92. Upper bollinger is 26467, and rising 375/400pts a week. As of next Monday's open, the 26700/800s will be technically on offer. Any price action above the next Fibonacci extrapolation of 26702 (the 26800s to be decisive) would be very significant, and give confidence we'll see sp>3100s this year, and that will then offer next grand target of the sp'3900/4000 zone in 2019.

NYSE comp'

The master index climbed for a TENTH consecutive week, settling +1.9% at a new historic high of 13637. The 14000s are on the menu into early spring. 15k seems a given later this year, with the 16000s viable for year end.

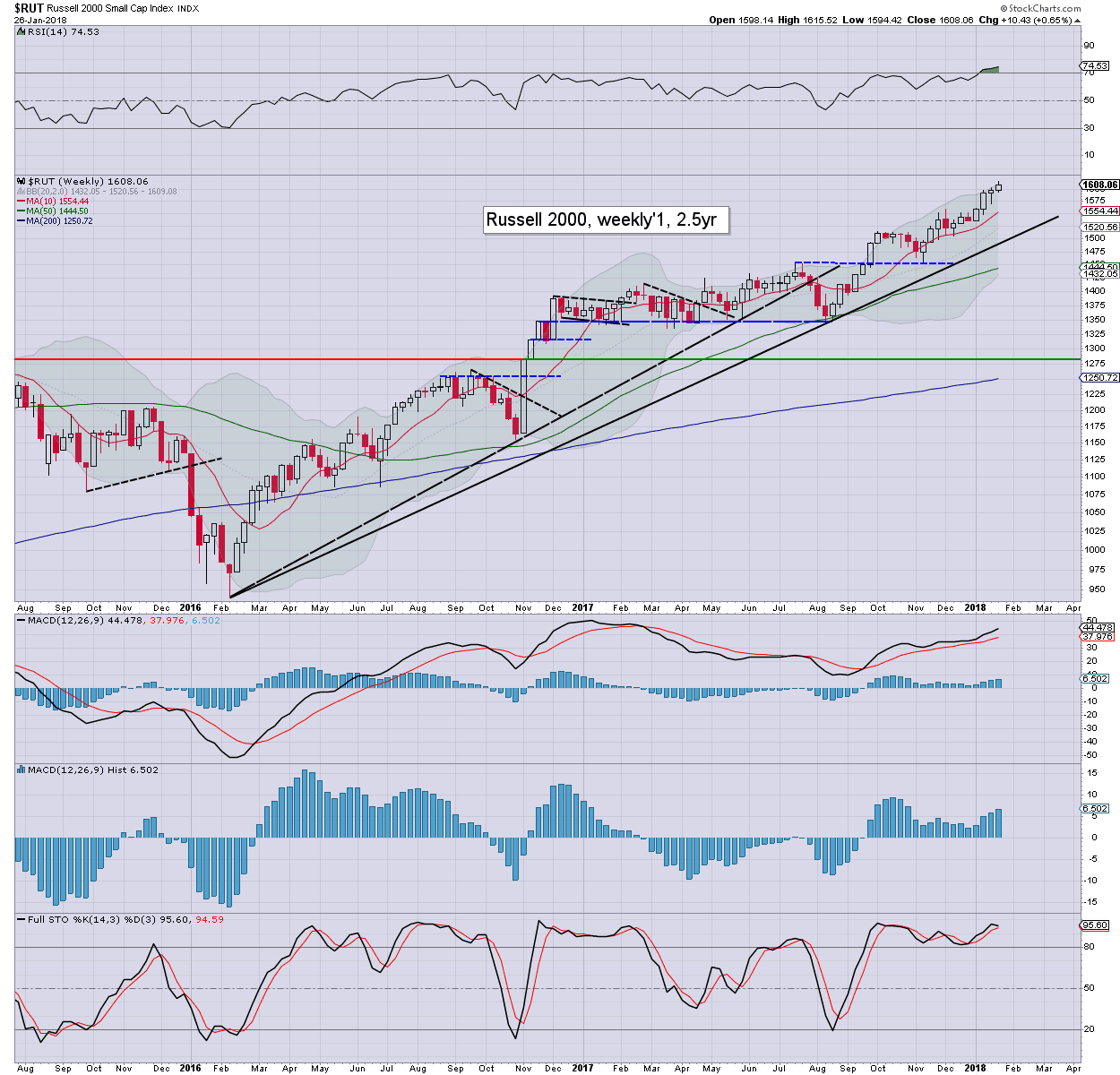

R2K

The second market leader - R2K, settled +0.6% at 1608, having broken a new historic high of 1615. The 1650/1725 zone appears due into the spring, before a correction is probable.

Trans

The 'old leader' struggled, settling lower for a second week, -1.6% at 11125. The airlines were hit hard this week on chatter that a price war via higher capacity is likely. Sustained higher oil/fuel prices are clearly not helping either. On balance though, recent cooling is arguably to be seen as sporadic, much like last Oct'/Nov.

--

Summary

Five of the six main indexes broke new historic highs, only the Transports missed out.

Relative strength and price momentum in some indexes is the highest since (at least) 1980.

Other than the Transports, there is no sign of a key m/t top, that would threaten even a relatively moderate 5% correction.

sp'daily6 - YTD price performance

Barely one full month of the year, and the Nasdaq comp' is net higher by a powerful 8.7%. The Dow is +7.7, with the sp' +7.4%. The Transports has notably swung from a leader to a laggard, mostly a result of the (unjustified) smack down in the airline stocks.

--

Looking ahead

As well as further earnings...

M - Pers' income/outlays

T - Case-Shiller HPI, consumer con'

9pm EST: Pres' Trump will give the State of the Union address to a joint session of congress. No doubt, Trump will refer to the hyper strong equity market, and how 'all your 401ks make your seem like financial experts'. I would look for some talk about an infrastructure bill. That would likely offer a major boost to certain materials and construction stocks at the Wednesday open.

--

W - ADP jobs, employment costs, Chicago PMI, pending home sales, EIA Pet' report

The FOMC will issue an press release at 2pm. No rate hike/policy change can be expected. There will not be a press' conf.

T - Weekly jobs, vehicle sales product/costs, PMI/ISM manu', construction

F - Monthly jobs, consumer sent', factory orders.

*the only fed official schedule is Williams on Fri, but it will be of no relevance.

--

If you value my work, subscribe to me.

For details:

https://permabeardoomster.blogspot.co.uk/p/subscriptions.html

Have a good weekend

--

*the next post on this page will likely appear 6pm EST on Monday.