It was a very bullish week for US equity indexes, with net weekly gains ranging from 2.4% (Trans), 1.0% (sp'500), to 0.8% (NYSE comp'). Near term outlook offers another 1-2% of basic upside. The only issue is when the first correction - since the Nov'/election low of 2083, occurs. The broader outlook remains powerfully bullish, at least to the 2400/500s by late summer.

Lets take our regular look at six of the main US indexes

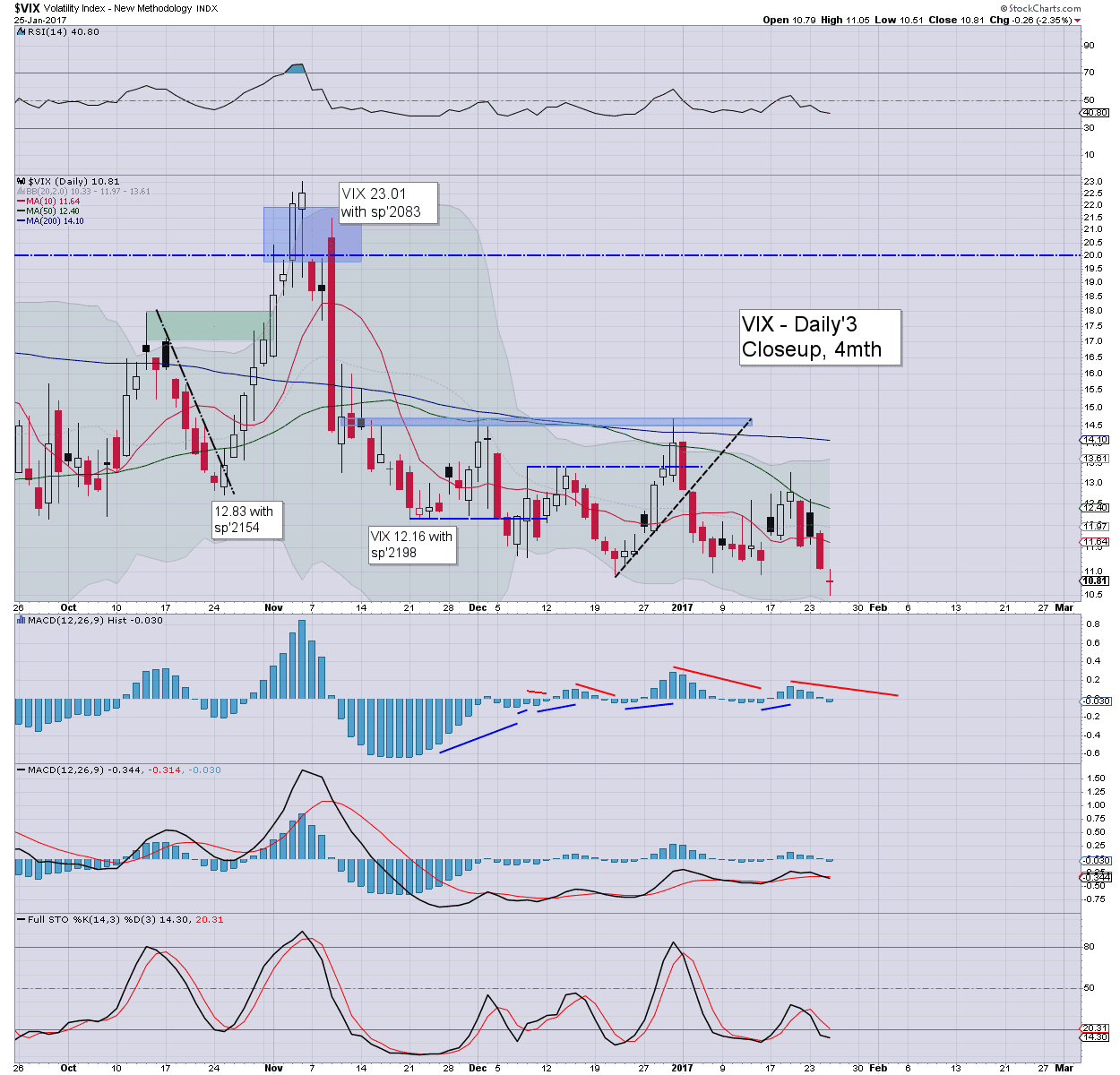

sp'500

A new historic high of 2300, with the sp' net higher by 23pts (1.0%), settling @ 2292. Underlying MACD (blue bar histogram) cycle is still leaning on the downward side, whilst new highs are still being made.

Best guess: a short term top around 2320/30s by mid Feb', and then a retrace of 4-5% into early March. Certainly though, no price action under 2200. The 2400s seem a given by May/June.

Keep in mind my year end target of 2683, which I recognise could be seen as 'crazy talk', but if we reach the 2500s by late summer, my target will be on track.

--

Nasdaq comp'

The Nasdaq continues to lead the broader market higher, and saw a net weekly gain of 1.9%, settling at 5660. Just reflect on this... the Nasdaq has climbed 34% since the Feb'2016 low of 4209. Assuming a minor retrace in Feb/March, at the current rate, we'll see the 6000s by May. Once we're at 6k, its a curious thought that the market could see a 16% washout, and still maintain core support of the 5K threshold.

Dow

The mighty Dow climbed 266pts (1.3%), breaking a new historic high of 20125, settling at 20093. Upper weekly bollinger will be offering the 20600s next week. A valid scenario is that 20k is going to hold as short/mid term support, and if the next retrace will be say... 5%... then we need to first climb to at least 21k, before the next retrace.

NYSE comp'

The master index gained 0.8%, with a new historic high of 11344, settling at 11283. The 12k threshold looks at least 3-4 months away. First support is the 11000/10900 zone, which looks secure into the late summer.

R2K

The second market leader - R2K, climbed by a rather significant 1.4%, settling at 1370. Upper bollinger will be offering the 1440/50s next week... which is a clear 4% higher. The 1500s seem due into the summer. Again, its a curious thought that few (if any) in the mainstream are talking about 'R2K @ 2k', before the current multi-year wave concludes.

Trans

The 'old leader' - Trans, was the leader this week, breaking a new historic high of 9502, settling with a net gain of 2.4% at 9444. Near term outlook is bullish to the 9700/800s. The 10k threshold looks out of range in the current run from early November.

--

Summary

All US equity indexes are broadly bullish, and holding near/at historic highs.

The Nasdaq continues to lead the way higher, with the Dow and sp' following. The R2K is a little laggy, but its price structure is a very clear bull flag.

Near term outlook is bullish, with another 1-2% of basic upside, before the next realistic opportunity of a 4-5% retrace.

--

Looking ahead

There is an absolute truck load of corp' earnings and econ-data in the week ahead...

notable corp' earnings: Tue': APC, AAPL, XOM, MA. Thurs: AMZN, DB. Fri': HSY, PSX.

M - pers' income/outlays, pending home sales

T - employment costs, case-shiller HPI, Chicago PMI, consumer con'

W - vehicle sales, ADP jobs, PMI/ISM manu', construction, EIA report

**FOMC announcement @ 2pm.There will not be a press' conf.

No one expects a rate hike, least of all yours truly. I remain expecting three rate hikes this year... May, Sept', and Dec'.

-

T - weekly jobs, product/costs

F - monthly jobs, PMI/ISM serv', factory orders

*as Tuesday is month end, expect price action to be pretty choppy across the afternoon, not least as the market might be a little twitchy ahead of AAPL earnings.

--

As ever, if you like these posts, you can support me via a monthly subscription. For $20pcm, you'll have access to my continued intraday postings, which total a rather monstrous 220/240 each month.

Have a good weekend

--

*the next post on this page will likely appear Mon' @ 7pm EST.